The global race for next-generation energy storage has reached a pivotal milestone. Dongfeng Motor, one of China's legacy automotive giants, has officially announced that its self-developed, next-generation Dongfeng solid state battery mass production phase will begin vehicle integration in the second half of this year. This aggressive timeline threatens to disrupt the roadmap of Western automakers still struggling to transition solid-state technology out of laboratory environments.

Under the Hood: Dongfeng's Oxide-Polymer Battery Tech

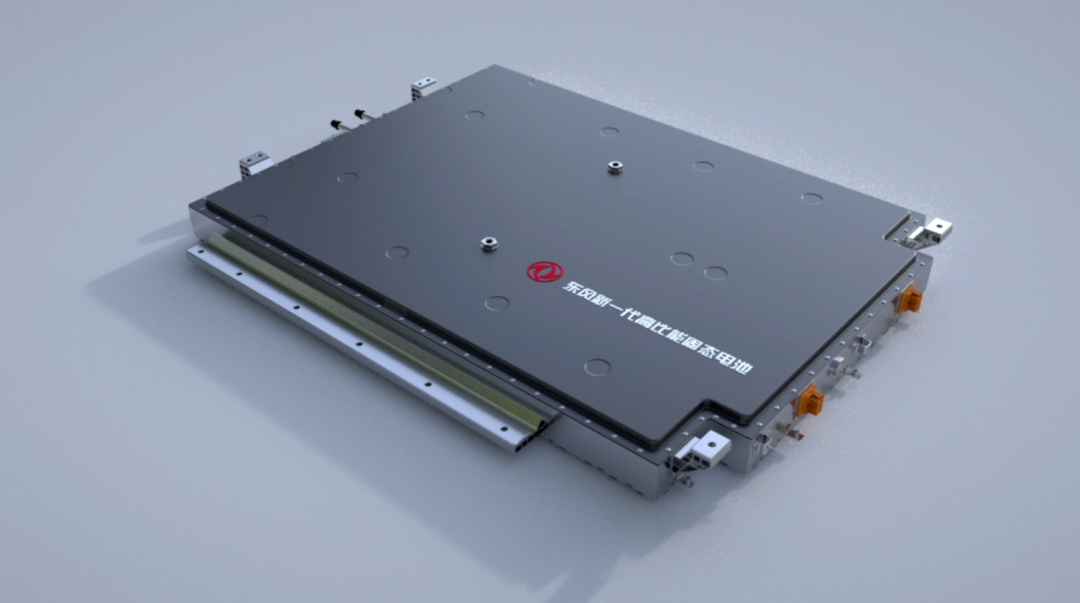

Unlike many Western competitors focusing heavily on sulfide-based solid-state electrolytes (which are highly conductive but notoriously difficult to manufacture and moisture-sensitive), Dongfeng has taken a pragmatic approach. Since 2018, their dedicated research team has focused on an oxide-polymer composite route.

This composite architecture offers several key advantages:

- Superior Thermal Stability: The high-safety solid electrolyte mitigates the risk of dendrite formation and thermal runaway from the source.

- Volumetric Efficiency: Achieving higher energy density within the same physical pack volume compared to traditional liquid lithium-ion setups.

- In-House Control: Dongfeng has achieved 100% intellectual property ownership across the entire vertical stack—from electrode materials and solid electrolytes to full pack integration.

Crucially, Dongfeng's pilot workshop is already fully automated, executing over 20 processes including raw material feeding, coating, baking, and precision welding. This is not just a bench-top experiment; it is an active, scaled manufacturing pipeline ready for prime time.

China vs. Global Solid-State Battery Timelines

To understand why this matters to automotive strategists and institutional investors, we must look at the global commercialization timelines. While Toyota and QuantumScape (backed by Volkswagen) target 2027 to 2028 for true solid-state integration, Chinese players are executing at 'China-speed' today.

| Company / Consortium | Electrolyte Chemistry | Target Production Window | Status |

|---|---|---|---|

| Dongfeng Motor | Oxide-Polymer Composite | H2 This Year (Mass Production) | Pilot lines fully active, vehicle integration phase. |

| WeLion / NIO | Semi-Solid Oxide-Liquid | Already deployed (150 kWh pack) | Commercial fleet active in NIO EVs. |

| QuantumScape (VW) | Anodeless Solid-State (Ceramic) | 2026 - 2027 (Low volume B-samples) | Testing phase with PowerCo. |

| Toyota | Sulfide-based | 2027 - 2028 | Pilot-scale development. |

Strategic Implications: The Western OEM Blind Spot

Many Western auto strategists dismiss current Chinese solid-state achievements as 'semi-solid stepstones' rather than 'pure solid-state' systems. However, this is a dangerous strategic blind spot. By choosing a hybrid oxide-polymer chemistry, Dongfeng avoids the intense manufacturing fragility of pure sulfide/oxide ceramic lines while capturing 80% of the safety and density benefits today.

For investors seeking alpha, this means Chinese OEMs are capturing the actual operational, fleet-level data of next-gen batteries years before Western legacy OEMs. The continuous iteration of thermal management software and pack integration during this cycle will likely cement China's EV dominance for the next decade.